This post is part of our ultimate guide to moving to London as a graduate. Pals, if you don’t have a set plan for budgeting on a graduate salary by now, you’ll be deep into your overdraft before you know it. Let us help you with that.

Yes, the average salary in London may be significantly higher than the rest of the United Kingdom. However, any extra you may be earning gets swiftly snatched away by the Big Smoke’s monstrous costs of living. After rent, transport and your food shop, any notion of a ‘disposable income’ basically disappears. Well, no more of that. We’re going to show you a guide to surviving and thriving in London on a tiny budget. Because you can.

How much money are we working with here?

Right, so we’ll be giving you guys an adjustable template for budgeting in London later. For now, we’ll be working on an annual salary of ВЈ18,000 per calendar year. Why? Because that’s what I started with when I first moved to London, so I’d rather speak to you guys from experience. Plus, I’ll be able to show you if I could do it, you can do it too.

***Brief salary interlude***

It’s probably a wise idea to figure out if you will be paid fairly. Most entry-level roles on the Debut app are a minimum of ВЈ20,000 per year, which, to most would be an acceptable starting amount. Money is sometimes hard to talk about. However, asking some close friends about their starting salary in their respective line of work may be beneficial. Especially if they work in a similar industry. This way, you’ll be able to gauge whether you should accept a job offer. If they aren’t paying you at least enough to live comfortably but frugally, perhaps it’s best to reconsider accepting. This is entirely to your discretion.

How will your graduate salary be divvied up?

I’ve used Money Saving Expert’s Tax Calculator to figure out how ВЈ18,000 a year will work out. It’s a really useful tool to break your budget down, considering you’ll probably have a different amount to this.

Post National Insurance and income tax, it works out to a take-home pay rate of ВЈ15,521 a year, or ВЈ1,298 a month. According to the tool, ВЈ18,000 isn’t a high enough wage for me to start paying back my student loans – so keep that in mind when you’re calculating your budget.

Read more: Here’s what you need to know about the recent changes to the student loans

The basics are as follows.

Rent

In London, rent prices can be pretty astronomical. When I started out, I was lucky enough to start on a base rent of ВЈ500 in a spare room in Zone 4. On average, however, I would budget for ВЈ550-600 per month. (Unless you so happen to be rollin’ in some ?, this should still leave enough for everything else.)

Something to bear in mind is your house deposit. This will usually be a one-off payment, which is why we haven’t included it in the breakdown. The standard rate is equivalent to six weeks of your base rent though, so you’ll absolutely need to save up for that. Or, dip into your overdraft, which we advise you do only with serious caution.

ВЈ1298 – ВЈ650 = ВЈ698 left.

Bills

Electricity, gas, water, Internet, council tax are the usual suspects. Negotiating these down to as low as possible can be really tricky depending on your housing situation. In my experience, this is usually around ВЈ100-ВЈ200 at most.

ВЈ648 – ВЈ150 = ВЈ548 left.

Transportation

It’s London, so more likely than not, you’ll be commuting on public transport. So, the Tube, local buses, and Santander cycles – heck, even boats if you’re feeling fancy. Transport for London have daily and weekly capping for those who use contactless and Oyster cards. Dependent on which zone of London you live in, this can vary, so take a look at their fares table to work out your transportation costs.

Our biggest transportation saving hack? Connecting your 16-25 National Railcard to your Oyster card to get a 34% discount on off-peak travel. You won’t save money during your commute, but you will on weekends.

ВЈ548-ВЈ181.70 (Zone 1-4 Travelcard) = ВЈ366.30 left.

Groceries and Household

Toto, something tells me we’re not living in halls anymore. A goodbye to cleaners and catered halls might be a shock to the system for some. Or for others who lived in private housing, this may be a great opportunity to, err, not live in a student-y home anymore. I was extremely careful with my groceries and household spending, which usually averaged at ВЈ25-30 a week.

ВЈ366.30 – ВЈ120 (ВЈ30 x 4 weeks) = ВЈ246.30 left.

Eating Out, Entertainment, Shopping

Yo, so London is expensive. We can’t police what y’all want to do, but we’d encourage that you don’t blow your entire monthly paycheck. Be selective of what you do, and work hard to find deals if you can. We recommend London On The Inside, Mr Hyde, Time Out, and London Cheap Eats as our top resources for finding the best ways to save and have fun in the Big Smoke.

ВЈ246.30 – ВЈ120 (aim for this number) = ВЈ126.30 left.

Savings/Emergency buffer

This should theoretically leave you with ВЈ126.30 of your paycheck left to save every month. Theoretically. Of course, things change month to month so you may not hit that number. Or, you might end up having a particularly frugal month and have more to put away.

We recommend opening up a savings account to squirrel this money away. This means there will be less temptation for you to dip into these funds as they won’t be as easily accessible. Set a reminder on your phone or email calendar for you to transfer funds into this account. Once you’ve done this a few times it should form a habit.

ВЈ126.30 – ВЈ126.30 = ВЈ0 left.

Top saving tips

The ‘basics’ range at supermarkets are going to be your new best friend.

As often as possible, go for own-brand products, which are often a LOT cheaper than branded goods. From experience, Sainsbury’s own-brand products are particularly great, If you’ve got a Lidl or an Aldi close by, even better.

Check your balance, and often.

At university, I had the terrible habit of ignoring my bank account balance in fear of discovering just how in debt I actually was. Make it a habit to check your balance every week. The only time you should be afraid of your balance is if you don’t know what it is!

Get a coin bank.

And a big one you can’t easily open either. You’d be surprise at how much your spare change can rack up. All the better if you make a ‘rule’ for dropping money in the coin bank. For example, make it a swear jar!

Understand what you’re spending your money on.

Keeping track of your expenditure is absolutely key to saving more. Make an Excel spreadsheet and tag each transaction with a category. Then you’ll be able to set targets on which area you should be reducing your expenditure in.

Get out of your overdraft as fast as you can.

If you’ve dipped into this at uni, your focus should be getting out of that debt as soon as possible. You might want to up your savings monthly target to make this happen, but your overdraft limit decreases each year you’re out of uni. Get on it, and don’t get penalised.

Don’t kick yourself if you fall off the saving wagon.

So, you might have spent a little too much money on a night out. It happens. Just tighten the belt, and try to make up the savings amount the next month.

A list of great tools to track your finances

Right pals. These three tools are basically your savings secret weapons. One’s a new kind of bank card, and two are actually Facebook Messenger chatbots. We’re living in the 21st century after all, and your budgeting should absolutely reflect that.

Monzo

Meet Monzo. Monzo is a sassy pink debit card coupled with the smartest banking mobile app we’ve ever seen.

What we love about Monzo is their instant payment notifications. Every transaction you make using the Monzo card is tracked – and every time you pay for something, you get a push notification. That means it totally guilt-trips you every time you pop into Primark and leave with ВЈ30 of stuff you don’t need. Thanks, Monzo!

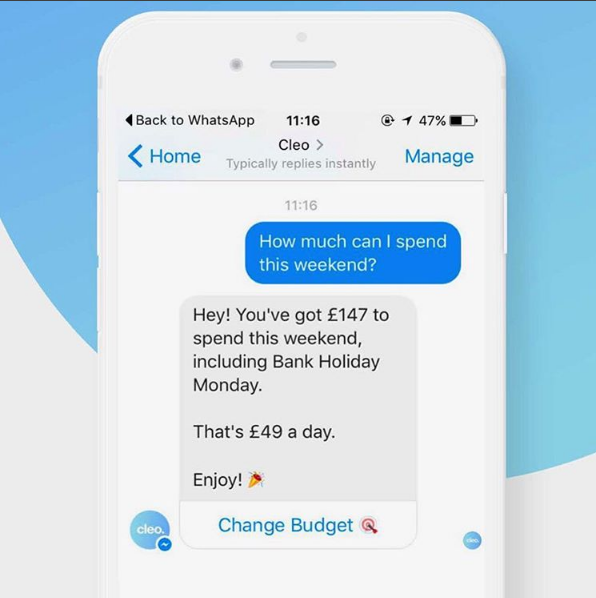

Cleo

We love Cleo, the smart financial dashboard for our generation. If you log on to the web dashboard, you get more financial insights than you can shake a stick at. You can:

- Set a monthly budget that’ll warn you if you’re about to exceed it.

- Get daily or weekly peeks into your spending activity

- It’ll tell you how much money you have left to spend until payday

And legit, like, so much more. You can add it to your Facebook Messenger for even more added convenience. Sweet.

Plum

Saving is hard, and tedious. It’s really easy to forget to put that important amount away each month, even with reminders. Plum is a really useful tool that takes the thinking outta your saving.

Essentially, you link your bank account to Plum, and it saves a small amount of money for you automatically. It squirrels it away into your Plum savings, away from your main account so you don’t accidentally spend it.

Like Cleo, you can also chat to Plum to find out more about your savings status. Plus, we love all the emojis they use to complement what could be really dull money statements.

And that, my friends, brings us to the end of our guide to budgeting on a graduate salary. Got any other tips? Tweet us @DebutCareers and we’ll add it to this post.

Check back next week for our next post in the guide:

Your no-nonsense guide to your renting rights in London